ALT/FNDATA · Alternative Assets

Q1 2026 Report: The Secondary Market for Luxury Handbags & Luxury Equity Performance

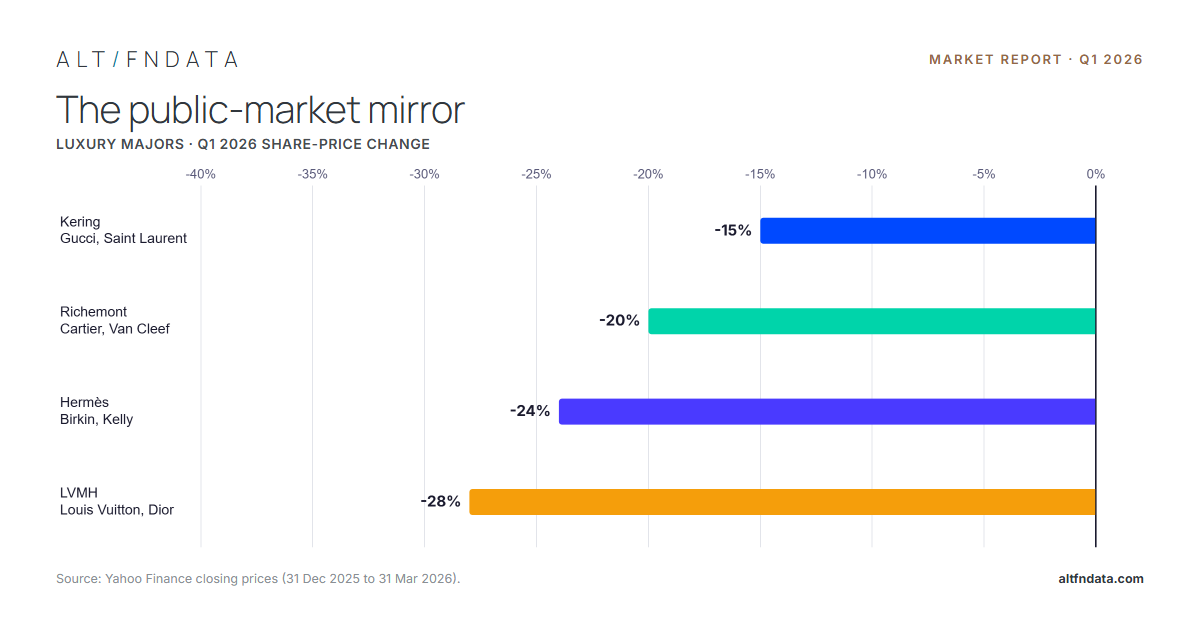

How the auction market and the listed luxury houses repriced together

Two markets, one shock. As luxury equities had their worst start to a year in over a decade, the secondary auction market repriced in lockstep — a real-time readout on luxury demand for allocators.

The headline

The correction in three numbers

−72%

Auction value, YoY

Total sold-auction value fell from $12.9M to $3.6M (−70% like-for-like)

−74.6%

Top-lot price

The quarter’s pinnacle fell from $275,675 to $69,850

−25%

Volume (like-for-like)

1,653 → 1,233 lots at houses tracked in both quarters; −32% across all

Auction-realized prices — what luxury actually sold for at the hammer, not asking prices. · 13M+ auction results · 100+ houses.

The read

What the data shows

The quarter reprices the category rather than empties it: value and the top end fell far harder than volume, which means the market sorted rather than collapsed. Speculative, trend-led pieces gave up their gains while Hermès Kelly and Birkin references held their bid, so for a buyer or a holder the signal is plain: the foundational blue chips carry value through a demand shock, while the pieces that ran hardest on the way up give it back.

Free report

Read the full report

Enter your email to unlock the full report, it’s free to read and yours to revisit anytime in your account.

- The luxury-equity table (LVMH, Hermès, Richemont, Kering) and the auction↔equity correlation

- Month-by-month liquidity & capital-deployed data (Jan → Mar)

- Concentration: brand hierarchy, house share, and where capital actually cleared

- The pinnacle-lot repricing, full year-over-year drawdown, and methodology

Please enter a valid email address.

Your report is unlocked

We’ve emailed you the executive summary and added you to the newsletter. Read the full report now — it’s yours anytime.

Read the full report →