ALT/FNDATA · Trade Briefing

Q1 2026 Report: The Secondary Market for Luxury Watches — A Dealer & Specialist Briefing

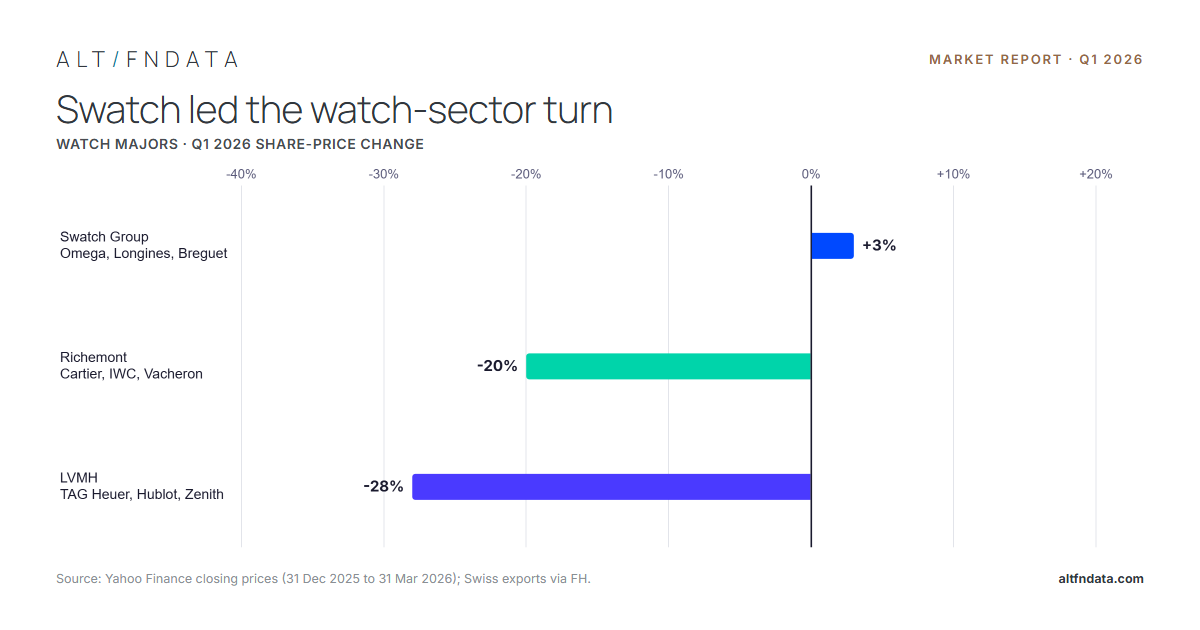

Auction-realized prices and the public-market backdrop

Where watches cleared in Q1 2026: the European mid-market houses accounted for the activity, the blue-chips set the ceiling, and the macro backdrop turned supportive for consignors.

The headline

The correction in three numbers

+1.4%

Swiss watch exports, Q1 YoY

The first positive quarter after a prolonged decline — the worst looks over

Flat→up

Like-for-like auction value

Stable at houses tracked in both quarters (+22% capital); the gross drop is a coverage shift

$45,204

Top lot — a Cartier Tank

Blue-chips set the ceiling; a deep base of vintage and unbranded sets the floor

Auction-realized prices — what watches actually sold for at the hammer, not asking prices. · 13M+ auction results · 100+ houses.

The read

What the data shows

The signal here is a turn, not another leg down: Swiss exports returned to growth for the first time in over a year and the listed houses rallied on the view that the cycle has troughed, while like-for-like auction value held flat to up (the headline gross decline is a coverage artifact, not a real one). For a buyer, the tell is what anchored every sale: classic, wearable references like Cartier, Rolex and Patek rather than speculative modern steel, which is where value holds when a cycle turns.

Free report

Read the full report

Enter your email to unlock the full report, it’s free to read and yours to revisit anytime in your account.

- The full month-by-month auction breakdown (January → March)

- The macro backdrop — Swiss exports, tariffs, the franc, Swatch & Richemont

- Brands & the blue-chip ceiling vs. the unbranded base

- Methodology, including a transparent note on coverage

Please enter a valid email address.

Your report is unlocked

We’ve emailed you the executive summary and added you to the newsletter. Read the full report now — it’s yours anytime.

Read the full report →